Divorce is one of the most financially consequential events of your life, and most people do not realize that until it is too late to undo certain decisions. The legal process may end in months, but the financial choices you make during it can affect your life for decades.

The good news is that many of the most expensive divorce-related financial mistakes are also the most preventable. With the right preparation, the right team, and a clear understanding of the numbers, you can make decisions that support your long-term financial future, not just the terms of a settlement agreement.

Below are 10 of the most common and costly divorce financial mistakes, along with the strategies that can help you avoid them.

What’s at Stake Financially in Divorce?

The average American household going through divorce is dividing retirement accounts, home equity, investment portfolios, business interests, insurance policies, and shared debt, often all at once, under emotional stress, and with a legal clock ticking.

Studies consistently show that financial outcomes in divorce are heavily influenced by preparation and professional guidance. People who work with a Certified Divorce Financial Analyst (CDFA®) are significantly more likely to negotiate settlements that reflect true after-tax, after-cost value. Those who do not often discover costly mistakes only after the decree is finalized, when the decisions are legally binding and far more difficult to correct.

Mistake 1: Waiting Too Long to Get Organized

Why it costs you: Decisions made without complete financial information are almost always worse than decisions made with it. During a divorce, bad decisions can become permanent very quickly.

Many people wait until settlement discussions are already underway before pulling together their financial records. By that point, positions have hardened, timelines are compressed, and negotiating leverage is often limited.

What to do instead: Start gathering financial documents as soon as divorce appears likely. Your list should include:

- Federal and state tax returns (3 years minimum)

- All bank account statements

- Brokerage and investment account statements

- Retirement account statements (401(k), IRA, pension, deferred compensation)

- Mortgage documents and the most recent appraisal or estimate

- Business ownership records, K-1s, or partnership agreements

- Life, disability, and long-term care insurance policies

- Estate planning documents (wills, trusts, POAs)

- Loan agreements and current balances

- Social Security earnings statements (available at ssa.gov)

- Stock option, RSU, or deferred compensation plan documents

Having a complete financial picture before settlement discussions begin puts you in a much stronger position.

Mistake 2: Not Knowing the Full Marital Balance Sheet

Why it costs you: You cannot negotiate a fair settlement on assets you do not know exist, or do not know how to value properly.

Many people can estimate roughly what they own. Far fewer know exactly how assets are titled, what they are worth on an after-tax basis, or whether debts are considered joint or separate. That can lead to overlooked assets, missed liabilities, and settlement agreements built on incomplete information.

What to do instead: Build a complete marital balance sheet that includes every asset and every liability:

- Liquid assets: Checking, savings, money market accounts

- Investment accounts: Taxable brokerage accounts, mutual funds

- Retirement assets: 401(k), 403(b), IRA, Roth IRA, SEP-IRA, pension, deferred compensation plans

- Real estate: Primary home, vacation property, rental property

- Business interests: Closely held businesses, partnership interests, professional practices

- Insurance: Whole life or universal life cash values

- Deferred compensation: Stock options, RSUs, restricted stock, ESPP shares

- Liabilities: Mortgages, HELOCs, auto loans, student loans, credit card balances, business debt

Don’t assume your spouse’s disclosure is complete. Cross-reference tax returns, credit reports, and W-2s to identify accounts or income streams that may be missing.

Mistake 3: Mistaking “Equal” for “Fair”

Why it costs you: A 50/50 split may look balanced on paper, but not all assets carry the same real-world value.

A settlement that gives you 50% of the assets can still leave you financially vulnerable if your share is illiquid, heavily encumbered, tax-inefficient, or poorly aligned with your actual financial needs. This is one of the most common and most overlooked financial mistakes in divorce.

What to do instead: Evaluate every proposed settlement against three key questions:

- What is the after-tax, after-cost value of what I’m receiving?

- Does this asset match my liquidity needs in the next 1–5 years?

- Does this settlement support my long-term financial plan, not just the numbers on the final settlement paperwork?

For example, accepting more home equity in exchange for less retirement savings can create serious cash flow issues, especially if housing costs are high and retirement is still many years away. Cash and a taxable brokerage account are not equivalent to a traditional 401(k) with the same balance, even if the statement values appear identical.

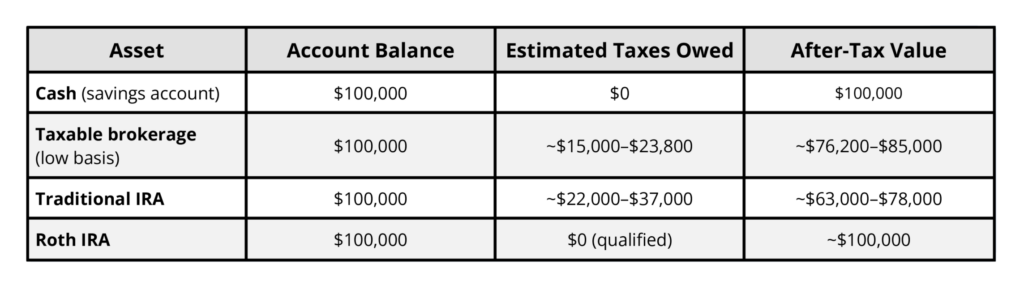

Mistake 4: Ignoring Taxes When Comparing Assets

Why it costs you: Two assets with the same account balance can have dramatically different after-tax values, and that difference ultimately comes out of your pocket.

Under federal law, transfers of property between spouses or former spouses incident to divorce generally do not trigger immediate recognition of gain or loss. However, that does not mean the tax liability disappears. In many cases, the receiving spouse also receives the asset’s tax basis and the future tax consequences that come with it.

Real-World Example:

What to do instead: Never compare assets based solely on statement balances. Work with a CDFA® or CPA to evaluate the after-tax value of each asset before agreeing to a settlement. Depending on the assets involved, the difference can amount to tens of thousands of dollars.

Mistake 5: Mishandling Retirement Account Division

Why it costs you: Retirement accounts are often the single largest asset in a divorce. They come with more rules, more complexity, and more ways to make expensive mistakes than almost any other asset class.

The key rules to understand:

Employer-sponsored plans (401(k), 403(b), 457, pension): These require a Qualified Domestic Relations Order (QDRO) — a separate court order directed to the plan administrator. Without a properly drafted and approved QDRO, the plan is not legally required to pay the alternate payee, even if the divorce decree mentions the account. QDRO errors and delays are among the most common and the most expensive post-divorce financial surprises.

IRAs (Traditional, Roth, SEP, SIMPLE): These do not require a QDRO. Instead, the IRS states that an IRA transferred to a spouse or former spouse under a divorce decree or written separation agreement incident to divorce is treated as the recipient’s own IRA, and the transfer itself is not a taxable event. However, the transfer must be handled correctly; a cash distribution to one spouse who then writes a check to the other spouse is taxable and may be subject to early withdrawal penalties.

Pensions: Defined benefit plans require special attention to actuarial valuation. The present value of a future pension payment must be calculated to compare it fairly against other assets. This calculation varies dramatically by age, years of service, discount rate assumptions, and survivor benefit elections.

What to do instead: Engage a QDRO specialist alongside your divorce attorney. Review every retirement account type separately. Never treat them as equivalent just because the balances appear similar.

Mistake 6: Failing to Build a Realistic Post-Divorce Budget

Why it costs you: A settlement can look completely reasonable on paper and still fail in real life if you haven’t modeled what your actual monthly finances will look like once one household becomes two.

Common post-divorce expenses people underestimate or miss entirely:

- Housing costs: Mortgage or rent, utilities, insurance, maintenance on a sole-owned home

- Health insurance: Loss of spousal coverage is one of the most significant and underestimated expenses

- Childcare: Full costs, not the portion previously shared

- Debt service: Car loans, student loans, and credit cards that may now be solely your responsibility

- Taxes: Single filing status, no longer sharing deductions

- Lifestyle adjustments: Subscriptions, memberships, and services previously split

What to do instead: Before agreeing to any settlement, especially around keeping the family home, build a line-by-line monthly budget reflecting your projected sole income, sole expenses, and new tax situation. If the numbers don’t work on paper, they won’t work in real life. A CDFA® can model multiple settlement scenarios against your projected cash flow to show you which one is actually sustainable.

Mistake 7: Overlooking Tax Filing Changes and Old Tax Liability

Why it costs you: Your tax situation changes completely with divorce, and past joint filings can follow you for years if you don’t address them.

Filing status: IRS Publication 504 specifies that your filing status is determined by your marital status on the last day of the calendar year. If your divorce is final on December 31, you file as single (or head of household, if eligible) for that entire tax year. If it is finalized on January 1, you may still file jointly for the prior year, with all the joint liability that entails.

Old joint returns: Divorce does not automatically sever liability for prior joint returns. The IRS can hold both former spouses jointly and severally liable for tax, interest, and penalties on any return filed while married. This means if your ex-spouse underreported income on a joint return five years ago, you may still be on the hook unless you qualify for Innocent Spouse Relief under IRC Section 6015.

Alimony: For divorces finalized after December 31, 2018 (under the Tax Cuts and Jobs Act), alimony payments are no longer deductible by the payer or included in income by the recipient. This changes the calculus significantly versus pre-2019 agreements.

What to do instead: Engage a CPA during the divorce process, not just after. Review prior joint returns for accuracy, understand your exposure, and model your new projected tax picture under both settlement scenarios before agreeing to terms.

Mistake 8: Moving Money or Assets Without Guidance

Why it costs you: Transfers, withdrawals, or large purchases made during divorce proceedings can violate court orders, trigger tax events, create dissipation claims, and damage your credibility with the judge, all at the worst possible time.

Even well-intentioned moves, like moving your direct deposit to a personal account, refinancing a joint vehicle into your name, or making a large home repair, can create legal and financial complications if done unilaterally during active proceedings.

What to do instead:

- Consult your attorney before moving, transferring, or encumbering any significant asset while the divorce is pending

- Document every transaction and its purpose in writing

- Establish your own individual bank account and credit profile, but do so transparently and with counsel

- Avoid large discretionary purchases that could be characterized as dissipation of marital assets

The credibility and goodwill you preserve by moving deliberately instead of reactively are worth far more than any short-term move you might make under stress.

Mistake 9: Forgetting Beneficiaries and Estate Documents

Why it costs you: A finalized divorce does not automatically update your beneficiary designations, and in most cases, it does not invalidate your existing will, trust documents, or powers of attorney. If you die before updating these, assets may pass to your ex-spouse regardless of your intent.

Documents that must be reviewed and updated post-divorce:

- Retirement account beneficiary designations (401(k), IRA, pension)

- Life insurance beneficiary designations

- Transfer-on-death (TOD) and payable-on-death (POD) account registrations

- Will and any testamentary trusts

- Revocable living trust (trustee designations, successor trustee, beneficiaries)

- Durable power of attorney

- Healthcare proxy / medical power of attorney

- HIPAA authorization forms

Note on federal preemption: Beneficiary designations on ERISA-governed plans (most 401(k) plans) are governed by federal law, which may override state law divorce decrees. The only way to be sure an ex-spouse will not receive your 401(k) is to change the plan designation directly with the administrator.

What to do instead: Create a post-divorce estate planning checklist before your decree is final and schedule an estate planning review within 60 days of finalization. This is not an optional administrative cleanup; it is essential for financial protection.

Mistake 10: Missing Social Security Opportunities

Why it costs you: Social Security benefits based on an ex-spouse’s earnings record can represent significant lifetime income. Many divorcing spouses never claim them, simply because they don’t know the rules.

Key Social Security rules for divorced spouses:

- The 10-year rule: If you were married for at least 10 continuous years before divorcing, you may be eligible to claim Social Security retirement benefits based on your ex-spouse’s earnings record, even if they have remarried. The benefit is up to 50% of the ex-spouse’s full retirement age benefit, and claiming it does not reduce your ex-spouse’s benefit in any way.

- Survivor benefits: If your ex-spouse dies, you may qualify for a survivor benefit of up to 100% of their benefit if you were married for at least 10 years and meet age and other eligibility requirements.

- Remarriage rules: If you remarry before age 60, you generally lose eligibility for divorced spouse survivor benefits. If you remarry at or after age 60, eligibility may be preserved. These thresholds matter enormously in long-term planning.

- Earnings record comparison: SSA pays the higher of your own earned benefit or the divorced spouse benefit — not both. But if your ex-spouse was the higher earner, this can meaningfully increase your projected lifetime income.

What to do instead: Obtain your Social Security earnings statement and, if you were married close to or beyond 10 years, model the long-term retirement income implications of both your own record and potential divorced spouse benefits before finalizing any settlement.

Your Divorce Financial Planning Checklist

Use this checklist to stay ahead of the most common mistakes:

Before settlement:

- Gather all financial documents (3 years’ tax returns, all account statements, loan docs, insurance policies)

- Build a complete marital balance sheet, including all assets and liabilities

- Calculate the after-tax, after-cost value of every major asset

- Review all retirement accounts and identify which require a QDRO

- Model a realistic post-divorce monthly budget

- Consult a CPA about prior joint return exposure and new filing status

- Review Social Security earnings record and projected benefits

After finalization:

- Update all beneficiary designations (retirement accounts, life insurance, TOD/POD accounts)

- Revise will, trust, power of attorney, healthcare proxy

- Confirm QDRO filing and plan administrator approval

- Adjust tax withholding for new single filing status

- Establish individual credit profile and close or refinance joint accounts

- Review health insurance coverage and COBRA or marketplace options

- Schedule annual financial plan review

Working With a CDFA® During Divorce

A Certified Divorce Financial Analyst (CDFA®) is a financial professional specifically trained to analyze the financial aspects of divorce. Unlike a general financial advisor, a CDFA® understands QDRO rules, tax basis implications, post-divorce cash flow modeling, and settlement scenario analysis, and works alongside your attorney to help you make financially sound decisions, not just legally permissible ones.

If you are going through a divorce and want to understand the true financial impact of your options before agreeing to anything, that is exactly the conversation we have at Finivi.

This article is provided for informational and educational purposes only and does not constitute legal, tax, or financial advice. The information contained herein is general in nature and may not apply to your specific situation. Divorce involves complex legal, financial, and tax considerations that vary based on individual circumstances, state law, and applicable federal regulations.

The content in this article should not be construed as a solicitation or offer to buy or sell any security or financial product, nor should it be interpreted as personalized financial, legal, or tax advice. You should consult with a qualified attorney, CPA, and financial advisor before making any decisions related to divorce proceedings or settlement agreements.

References to tax rules, IRS publications, Social Security Administration guidelines, and retirement account regulations are provided for general informational purposes only and are subject to change. Finivi does not provide legal or tax advice. Tax and legal information discussed in this article may not reflect the most current developments and should be verified with appropriate professional counsel.

Certified Divorce Financial Analyst (CDFA®) is a professional designation granted by the Institute for Divorce Financial Analysts (IDFA). Use of this designation does not imply a specific level of investment or advisory services.

You must be logged in to post a comment.